Email marketing for financial advisors is the use of permission-based email to nurture prospects, stay close to existing clients and earn referrals, inside the rules the SEC and FINRA set for adviser advertising. It fits the business well. Money decisions are slow and trust-led and a client who reads your monthly note for a year is the one who moves their portfolio to you or sends their sister.

I have built email programs in several regulated and unregulated spaces. Finance is its own animal. The tactics that grow a list are the same everywhere, but advisors carry a compliance layer that a generic email guide will never mention. Get that part wrong and the cost is an SEC examiner, not a low open rate. This guide covers both halves: what grows the business and what keeps you compliant in 2026.

Why email is a strong channel for advisors

The trust gap email closes

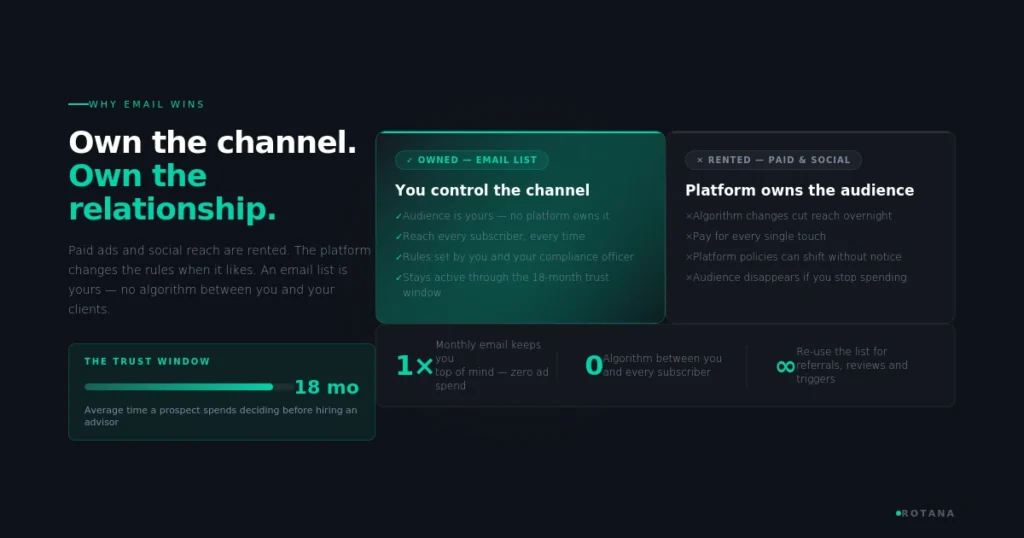

Financial advice is a considered purchase. Prospects rarely hire on first contact. They watch, they read, they wait until a life event forces a decision. Email is the only channel that lets you stay present through that whole window without paying for each touch. A consistent, useful email keeps you in mind for the eighteen months a prospect spends deciding.

Why owned audiences beat rented ones

Paid ads and social reach are rented. The platform owns the audience and changes the rules whenever it likes. An email list is yours. For a practice built on long relationships and referrals, owning the channel that carries those relationships is worth more than chasing reach you do not control.

The compliance layer that changes everything

This is the part that separates advisor email from every other industry. If you are an SEC-registered investment adviser, your marketing is governed by the SEC Marketing Rule and email is marketing.

What the SEC Marketing Rule requires

The Marketing Rule is Rule 206(4)-1 under the Investment Advisers Act of 1940. The SEC modernized it in 2020 and it became fully enforceable on November 4, 2022, merging the old advertising and cash-solicitation rules into one principles-based framework. Under the rule, advisers must avoid false or misleading statements, present fair and balanced information rather than cherry-picking the upside, avoid specific guarantees or promises and disclose conflicts of interest. Those principles apply to the words in your emails the same as any other ad.

The testimonial and endorsement trap

The rule now permits testimonials and endorsements, which the old rule banned, but with conditions. If a person is compensated for a testimonial, that must be clearly disclosed, even when the compensation is non-cash. An adviser using testimonials must oversee compliance and, in most cases, have a written agreement with the person giving it. There is a carve-out: the written-agreement requirement does not apply where the promoter is an affiliate whose status is disclosed, or where compensation is de minimis, which the SEC sets at $1,000 or less over the prior twelve months. So a client quote in your newsletter is allowed, but only handled correctly.

Why 2026 raises the stakes

This is not a dormant rule. The SEC’s Division of Examinations released a Risk Alert in December 2025 signaling that client testimonials, endorsements and third-party ratings are a focus of adviser examinations in 2026. The Staff said it expects upfront disclosures, proactive diligence and documented compliance across marketing. By April 2024 the SEC had already reported widespread deficiencies, including unsubstantiated claims and unbalanced presentations. Reviewing your email templates and any dated testimonials before an examiner does is the prudent move this year.

Recordkeeping you cannot skip

The amended recordkeeping rule, 204-2, requires advisers to make and keep copies of all advertisements they disseminate, directly or indirectly. Your marketing emails count. Keep them. If you are a broker-dealer or dually registered, FINRA Rule 2210 on communications with the public applies on top of this, with its own content and retention standards.

One caveat for this whole section. I am a marketer, not a compliance lawyer. Treat this as the lay of the land, then run your templates past your compliance officer or counsel before sending. The rules reward advisors who build compliance in from the start rather than bolting it on after a deficiency letter.

Build a compliant list the right way

Where the best subscribers come from

Permission is the foundation and for an advisor it doubles as a compliance and deliverability safeguard. Your strongest list is built from people who already know you: current clients, past clients and prospects who opted in after a meeting or a download. Add an opt-in to your client onboarding. Offer a genuinely useful resource on your site, a retirement-readiness checklist or a plain-language guide to a tax change. Capture email at reviews and events.

Why bought lists are a double risk

Buying a list is worse for advisors than for most businesses. It wrecks deliverability and violates platform terms like anyone else, but it also drags you toward marketing to people who never consented, which is the opposite of the fair-dealing posture the SEC expects. Build the list slowly and keep it clean.

The email sequences that grow a practice

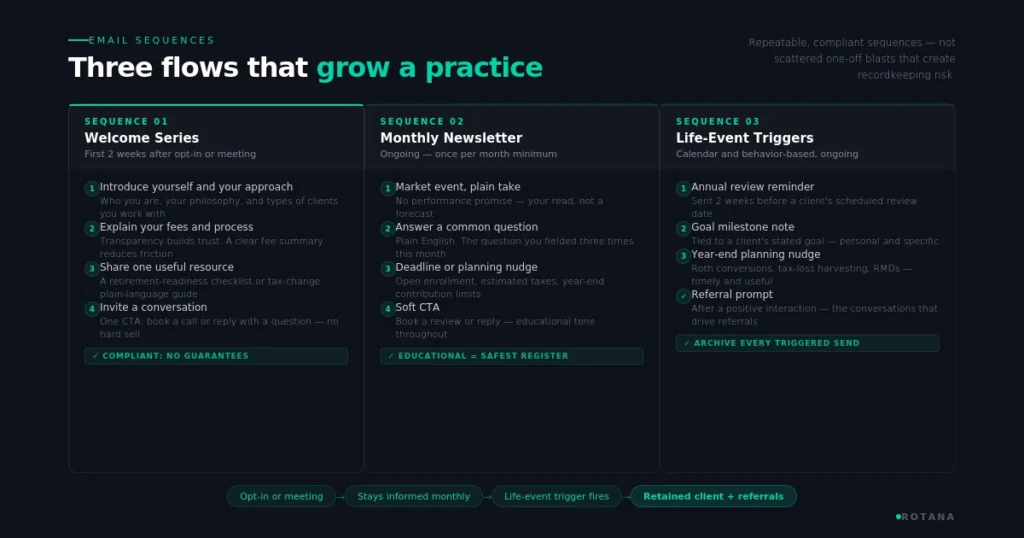

An advisor email program runs on a few dependable flows rather than scattered sends.

The welcome sequence

The welcome sequence is the highest-value place to start. When a prospect joins your list, a short series over the first two weeks introduces you, explains your approach and your fees, shares one useful resource and invites a conversation. This is where a cold subscriber becomes someone who books a call.

The ongoing client newsletter

A monthly newsletter keeps you present across the long decision window. Lead with what the reader can use: a clear take on a market event without a performance promise, an answer to a question you field constantly, a reminder about a deadline like open enrollment or estimated taxes. Keep it educational. Educational content sidesteps most of the misleading-claim risk while building the trust that drives referrals.

Life-event and review triggers

Behavior and calendar triggers do quiet, steady work. An annual review reminder, a note tied to a client’s stated goal, a year-end planning nudge. These feel personal because they are and they prompt the conversations that deepen a relationship without any hard sell.

Write advisor emails that land

Segment so the message fits

A pre-retiree and a young professional building their first portfolio need different emails. Segmenting by life stage, account type or stated goal lifts engagement and keeps each message relevant enough to stay on the right side of the fair-and-balanced standard.

Keep claims clean

Write plainly and avoid the phrasing that gets advisors in trouble. No guarantees, no cherry-picked returns, no implied promises. If you reference performance, the Marketing Rule has specific requirements, so that is a compliance-review item, not a casual line in a newsletter. Education is your safest and most effective register.

Measure what reflects real behavior

Open rates are now a soft signal because Apple’s Mail Privacy Protection inflates them. Track click-through rate, replies, review meetings booked and referrals generated. An advisor who books two review meetings from one newsletter has a better program than one chasing opens.

What I would do first

If you are an advisor starting from scratch, do three things this month. Turn your client and prospect contacts into a permission-based list. Draft a short welcome sequence and a monthly educational newsletter. Send both past your compliance officer before the first send, then watch clicks, replies and meetings rather than opens.

Email rewards consistency more than flair. The advisor who sends one genuinely useful, compliant email every month for a year builds a referral engine no ad campaign matches. If you want help building that system, including the compliance-aware templates and sequences, that is the kind of work I do at Rotana. You can book a call through the link on the site. If you are a finance lawyer or any kind of lawyer you can read our blog on email marketing for lawyers.

Frequently asked questions

Can financial advisors do email marketing?

Yes. Financial advisors are allowed to market through email, alongside websites and social media. SEC-registered advisers must follow the SEC Marketing Rule, Rule 206(4)-1, which requires fair, balanced and non-misleading communications and broker-dealers must also follow FINRA Rule 2210. Marketing to a permission-based list of clients and opted-in prospects, with compliant content, fits comfortably inside those rules.

Are client testimonials allowed in advisor emails?

Yes, since the 2020 Marketing Rule amendments, but with conditions. Compensated testimonials must disclose the compensation, even if it is non-cash and the adviser generally needs a written agreement with the person giving it unless they are a disclosed affiliate or paid a de minimis amount of $1,000 or less over twelve months. The SEC flagged testimonials and endorsements as a 2026 examination focus, so disclosures and documentation matter more than ever.

How often should a financial advisor email clients?

A monthly newsletter suits most practices. Financial decisions move slowly, so steady presence beats high frequency. One useful, educational email a month keeps you top of mind through a long decision window without overwhelming your list, supplemented by life-event and annual-review triggers as they arise.

Do advisors have to keep copies of marketing emails?

Yes. The amended recordkeeping rule 204-2 requires investment advisers to make and keep copies of all advertisements they disseminate, directly or indirectly and marketing emails count as advertisements. Retain your campaigns. Dually registered firms also fall under FINRA’s recordkeeping standards for communications.

What should financial advisors avoid in marketing emails?

Avoid anything false, misleading or unbalanced. That means no performance guarantees, no specific promises, no cherry-picking only the upside of a strategy and no undisclosed conflicts or paid testimonials. Cherry-picking and unsubstantiated claims are among the deficiencies the SEC has cited, so keeping emails educational and fair is both the safest and the most effective approach.